Core data

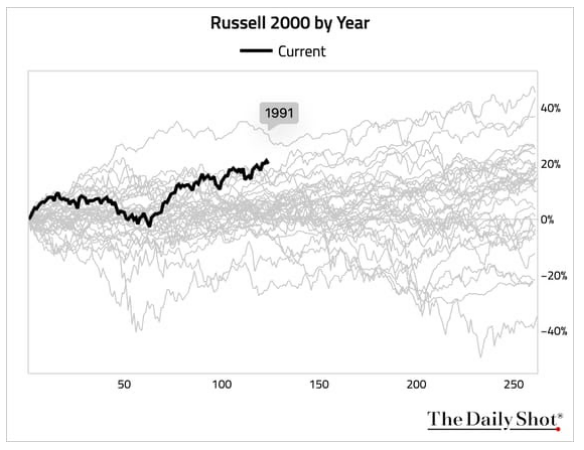

First half performance : Best since 1991Historical reference : First time in 35 years

Market Characteristics : Small-cap stocks surge across the board

Institutional warning : Risk of reversal exists in the second half of the year.

The craziest six months in 35 years

On Tuesday's close, the Russell 2000 index, representing small-cap stocks, locked in a historic milestone: this was the best performance for small-cap stocks in the first six months of the year since 1991. Keep in mind, in 1991, the internet wasn't commercialized, and smartphones were nothing new.How strong is this surge? A comparison will tell you: In the past 35 years, small-cap stocks have rarely finished the year's work in the first half of the year. In most years, they are either slow starters or simply sluggish throughout the year. But in the first half of 2026, small-cap stocks seemed to suddenly have a cheat code, leaving investors who were used to the steady returns of large-cap stocks dumbfounded.

Why small-cap stocks?

The surge in small-cap stocks didn't happen out of thin air. These companies typically have market capitalizations between $300 million and $2 billion, are more reliant on the domestic economy, and are extremely sensitive to interest rate changes. In early 2026, the market bet on a Federal Reserve rate cut, coupled with economic data showing stronger-than-expected domestic demand, naturally making these "high-beta" small-cap stocks the target of capital inflows. Another key factor was valuation repair. In the past few years, large-cap tech stocks have surged ahead, leaving small-cap stocks neglected and their valuations at historical lows. When market sentiment shifted, these "bargains" became sought-after targets. Funds withdrew from crowded sectors and flowed into undervalued corners, thus putting small-cap stocks in the spotlight.

But the second half of the year might be a different story.

The problem is that historical data shows the stronger the initial surge, the weaker the subsequent momentum tends to be. Analysts point out that in years when small-cap stocks perform so strongly in the first half of the year, they typically experience a correction or enter a period of volatility in the second half. The reason is simple: rapid gains have overdrawn future expectations and inflated valuations, leaving less room for further increases. Even more problematic is the uncertainty of the macroeconomic environment. If the Federal Reserve's interest rate cuts fall short of expectations, or economic data weakens, small-cap stocks, which are sensitive to interest rates and the economy, will be the first to be affected. Unlike large tech giants with global operations and ample cash flow as a moat, they will fall more sharply than large-cap stocks once market sentiment shifts. Another easily overlooked risk is liquidity. Small-cap stocks naturally have lower trading volumes than large-cap stocks. Once market volatility intensifies, buying pressure can dissipate very quickly, leaving investors unable to sell. This liquidity risk is not noticeable in a bull market, but it amplifies losses during corrections.Three signals to watch closely in the second half of the year

The Fed's policy shift and expectations of interest rate cuts are the core drivers of small-cap stock gains. If inflation rebounds or employment data overheats, and the Fed postpones rate cuts or even resumes rate hikes, the valuation logic for small-cap stocks will collapse instantly. Closely monitor each FOMC meeting and Powell's speeches.Corporate profit realization

The first half of the year saw price increases driven by expectations; the second half will depend on actual earnings. Earnings season is particularly crucial for small-cap companies: if revenue growth lags behind stock price increases, or if profit margins are eroded by costs, funds will withdraw without hesitation.Market volatility changes

When the VIX (Volatility Index) spikes, small-cap stocks are usually the first to suffer. They have poor liquidity and high volatility, making them prime targets for institutional selling when risk aversion intensifies. If the VIX breaks through 20, it's a warning sign.History doesn't simply repeat itself, but it always rhymes.

Looking back at similar market trends since 1991, small-cap stocks, after a strong start, showed significant divergence in performance in the second half of the year. In some years, the upward trend did continue, but more often it was a surge followed by a pullback, sometimes even erasing most of the gains from the first half of the year. The key variables have always been the macroeconomic environment and whether valuations are reasonable.The question now is: is this surge in the first half of 2026 the start of a new bull market, or just a short-lived rebound after a sharp decline? The answer may not be revealed until the third-quarter earnings season. Until then, the best thing investors can do is not be blinded by the impressive figures of the first half of the year, and always remember that risk and return are two sides of the same coin.

Frequently Asked Questions

What are the key differences between small-cap and large-cap stocks?Small-cap stocks typically refer to companies with a market capitalization between $300 million and $2 billion. They are more reliant on the domestic market, extremely sensitive to interest rates and economic cycles, and exhibit far greater volatility than large-cap stocks. Large-cap stocks, on the other hand, refer to companies with a market capitalization exceeding $10 billion. They often have global operations and stable cash flow, making them more resilient to risks, but their upside potential is relatively smaller.

Why do small-cap stocks perform well in the first half of the year but tend to fall in the second half?

Rapid price increases in the first half of the year often indicate that future expectations have been overdrawn, and the room for further growth is limited after valuations have been pushed up. At the same time, if the macroeconomic environment (such as interest rates and economic data) falls short of expectations, or if corporate profits fail to materialize, funds will quickly withdraw. Small-cap stocks have poor liquidity, and once sentiment shifts, their declines will be more severe than those of large-cap stocks.

Should ordinary investors chase after small-cap stocks now?

Chasing rallies requires extreme caution. Small-cap stocks are highly volatile and have poor liquidity, making them unsuitable for investors with low risk tolerance. If you already hold shares, consider taking partial profits to lock in gains; if you haven't entered the market yet, it's advisable to wait for a market correction or observe until the trend becomes clearer in the second half of the year before making a decision. Avoid blindly chasing rallies at historical highs.This page is for informational purposes only and does not constitute any investment advice. The market is risky, and investment requires caution. Any investment decisions should be based on your own financial situation, risk tolerance, and professional advice.